Europe Advanced Wound Care Market Outlook 2025–2032: Growth, Innovation & Opportunities

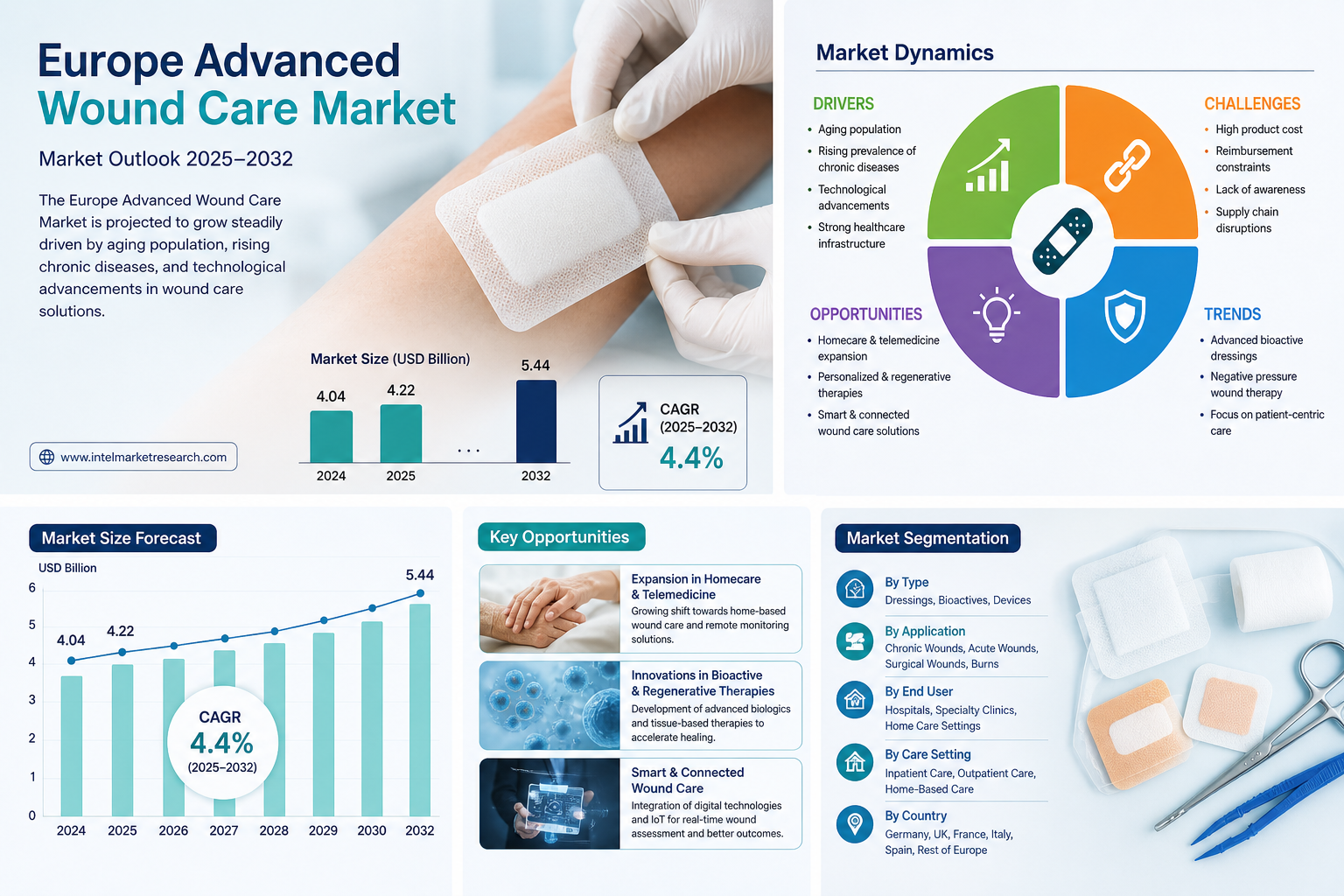

According to a new report from Intel Market Research, the Europe Advanced Wound Care Market was valued at USD 4.04 billion in 2024 and is projected to grow from USD 4.22 billion in 2025 to USD 5.44 billion by 2032, exhibiting a CAGR of 4.4% during the forecast period (2025–2032). This steady growth is underpinned by the region's rapidly aging population, a rising burden of chronic diseases such as diabetes and obesity, and well-established public healthcare systems that prioritize evidence-based wound management protocols.

What is Advanced Wound Care?

Advanced wound care encompasses a broad category of sophisticated medical solutions designed to treat complex, non-healing wounds that do not respond adequately to conventional therapy. These products operate on the clinically proven principle of moist wound healing, which accelerates tissue regeneration by maintaining an optimal healing environment at the wound site. The product landscape includes specialized dressings such as hydrogels, hydrocolloids, alginates, films, and foams, as well as bioactive products incorporating growth factors and collagen, and advanced therapy devices such as negative pressure wound therapy (NPWT) systems and electrical stimulation platforms. Their primary clinical functions include maintaining a stable periwound temperature, facilitating oxygen exchange, protecting against microbial infection, removing necrotic tissue, and minimizing patient discomfort during dressing changes.

This report provides a deep insight into the Europe Advanced Wound Care Market covering all its essential aspects-from a macro overview of the market to micro details such as market size, competitive landscape, development trends, niche markets, key drivers and challenges, SWOT analysis, and value chain analysis. The analysis helps the reader understand competition within the industry and strategies for enhancing profitability. Furthermore, it provides a framework for evaluating and assessing the position of a business organization. The report focuses on the competitive landscape of the European market, introducing market share, performance, product positioning, and operational insights of major players. In short, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those planning to foray into the Europe Advanced Wound Care market.

📥 Download Sample Report:

Europe Advanced Wound Care Market - View in Detailed Research Report

Key Market Drivers

1. Aging Demographics and Chronic Disease Prevalence

The primary engine for the Europe Advanced Wound Care Market is its rapidly aging population. In the European Union, over 20% of the populace is aged 65 and above-a cohort significantly more susceptible to chronic wounds including diabetic foot ulcers, venous leg ulcers, and pressure ulcers. This demographic shift creates a sustained and growing demand for effective wound management solutions that go beyond traditional gauze and bandages. The correlation is direct: as the population ages, the incidence of comorbidities such as diabetes and vascular diseases rises, further propelling the need for advanced therapeutic modalities across hospital, outpatient, and home care settings.

2. Technological Advancements and Product Innovation

Continuous innovation is a critical driver reshaping the European market. The sector is witnessing a surge in sophisticated products, including bioactive dressings, negative pressure wound therapy (NPWT) systems, and advanced cellular and tissue-based products. These innovations offer superior healing outcomes, reduced treatment times, and improved patient comfort compared to conventional methods. The integration of smart technology-such as biosensors embedded within dressings to monitor wound parameters in real time-represents the next frontier, enhancing treatment precision and adherence across the Europe Advanced Wound Care sector.

➤ The high and escalating cost of chronic wound management to European healthcare systems, estimated in the billions of euros annually, is a powerful incentive for adopting advanced wound care products that can reduce healing times, prevent complications, and lower overall treatment costs.

Furthermore, the expansion of outpatient and homecare settings across Europe, accelerated by healthcare decentralization policies and the need to manage hospital capacity more efficiently, is driving adoption of user-friendly and effective advanced wound care products suitable for non-clinical environments.

Market Challenges

High Product Cost and Reimbursement Hurdles

Despite their compelling clinical benefits, advanced wound care products face significant financial barriers to widespread adoption. These premium-priced therapies frequently encounter stringent and fragmented reimbursement landscapes across European countries. The absence of uniform reimbursement policies and the slow pace of inclusion into national health system formularies can restrict patient access-particularly for the most innovative and costly options such as bioengineered skin substitutes. This creates a persistent challenge for market penetration and sustained growth across the region.

Clinical Adoption and Training Gaps

Effective use of advanced wound care products often demands specialized clinical knowledge that is not uniformly distributed across the healthcare workforce. Inconsistencies in training and awareness among healthcare professionals-particularly in primary and community care settings-can lead to suboptimal product selection and application, undermining both clinical outcomes and cost-effectiveness. Addressing these education gaps remains an ongoing challenge for industry stakeholders and healthcare systems alike.

Supply Chain and Raw Material Dynamics

The Europe Advanced Wound Care Market is sensitive to disruptions in the supply of critical raw materials and components. Geopolitical tensions and logistical uncertainties can affect the production and timely availability of key products, while price volatility for specialized biomaterials adds meaningful pressure to manufacturing cost structures.

Market Restraints

Stringent Regulatory Frameworks and Approval Processes

The stringent regulatory environment in Europe, governed by the Medical Device Regulation (EU MDR), acts as a significant structural restraint on market dynamics. The MDR imposes rigorous clinical evidence requirements, heightened post-market surveillance obligations, and comprehensive quality management systems on all wound care product manufacturers. While these measures ultimately ensure patient safety and product quality, they extend product development timelines and substantially increase compliance costs. This regulatory burden can delay the introduction of new innovations to the Europe Advanced Wound Care Market and disproportionately affect smaller companies with limited R&D and regulatory resources, contributing to ongoing market consolidation among well-capitalized multinational incumbents.

Emerging Opportunities

Expansion into Homecare and Telemedicine Integration

The broad shift towards value-based healthcare and patient-centric care models presents a compelling opportunity for the Europe Advanced Wound Care Market. There is significant commercial potential for products and solutions specifically engineered for the homecare setting. The integration of advanced dressings with digital health platforms and telemedicine infrastructure allows for remote monitoring of wound healing progress, enabling timely clinical interventions while improving patient compliance and satisfaction. This aligns directly with European health policy priorities aimed at reducing hospital stays, managing escalating acute care costs, and empowering patients to manage their conditions with greater independence.

Personalized Medicine and Regenerative Therapies

The frontier of personalized wound care and regenerative medicine offers transformative growth potential for market participants. Advancements in areas such as 3D bioprinting of skin constructs, growth factor therapies tailored to individual patient profiles, and advanced antimicrobial strategies designed to combat specific pathogens are progressing steadily through clinical development pipelines. The development of these highly targeted solutions for complex, non-healing wounds represents a high-value segment that could redefine treatment standards and unlock premium pricing models within the European market over the coming years.

📥 Download Sample PDF:

Europe Advanced Wound Care Market - View in Detailed Research Report

Regional Market Insights

- Germany: Germany stands as the dominant force within the European advanced wound care market, driven by its highly developed healthcare infrastructure, robust reimbursement framework, and a strong culture of clinical innovation. The country's network of specialized wound care centers and outpatient clinics facilitates early adoption of cutting-edge therapies, including bioactive dressings, NPWT, and cellular-based products. Strong public and private investment in digital health and telehealth-supported wound monitoring is further reshaping care delivery models in Germany.

- United Kingdom: The United Kingdom represents a significant contributor to European market revenue, supported by the National Health Service's structured approach to wound management and emphasis on evidence-based clinical practice. Despite ongoing budget pressures within public healthcare, increasing recognition of the cost-effective outcomes associated with advanced wound care continues to drive procurement decisions. The growing home care and community nursing sector further expands the addressable market.

- France: France occupies a prominent position underpinned by its well-established healthcare system and strong physician awareness of advanced wound healing modalities. France's universal health coverage model facilitates access to premium wound care products, and government-backed initiatives aimed at reducing hospital-acquired infections continue to stimulate market growth.

- Italy: Italy's market is characterized by a significant burden of chronic wounds linked to its aging population and an evolving healthcare infrastructure progressively modernizing wound management practices. National clinical guidelines are helping to standardize care across the country's fragmented regional health system.

- Spain: Spain contributes meaningfully to the European landscape, driven by increasing awareness of chronic wound management and a growing geriatric demographic. Diabetic foot ulcer management has emerged as a key clinical priority, and global wound care companies are accelerating adoption through local distribution partnerships and clinical education programs.

Market Segmentation

By Type

- Advanced Wound Dressings (Hydrogels, Hydrocolloids, Alginates, Foams, Films)

- Bioactives (Growth Factors, Skin Substitutes, Collagen-based Products)

- Devices (Negative Pressure Wound Therapy, Electrical Stimulation, Hyperbaric Oxygen)

By Application

- Chronic Wounds (Diabetic Foot Ulcers, Venous Leg Ulcers, Pressure Injuries)

- Acute Wounds (Traumatic Injuries, Lacerations, Abrasions)

- Surgical Wounds (Post-operative Incisions, Donor Sites)

- Burns

By End User

- Hospitals

- Specialty Wound Care Clinics & Outpatient Centers

- Home Care Settings

By Care Setting

- Inpatient Care

- Outpatient & Ambulatory Care

- Home-Based Care

By Technology

- Conventional Advanced Dressing Technologies (Moisture-Retentive, Antimicrobial)

- Bioactive & Biological Technologies (Growth Factors, Skin Substitutes)

- Active & Smart Wound Care Technologies (NPWT, IoT-Enabled Dressings)

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Competitive Landscape

The European advanced wound care market, which accounts for over 33% of global revenue, is served by a concentrated group of multinational corporations with deep-rooted operational presence across Germany, the United Kingdom, France, and the Nordic countries. Market leadership is held by Smith & Nephew, Mölnlycke Health Care, ConvaTec Group PLC, 3M Company, and Coloplast A/S-companies that collectively command a significant share of the regional market through diversified portfolios spanning advanced wound dressings, NPWT systems, and bioactive products. Mölnlycke, headquartered in Gothenburg, Sweden, holds a particularly strong position in Europe owing to its regional origin and well-established relationships with European hospital procurement networks. ConvaTec has sustained competitive advantage through its focus on chronic wound management solutions aligned with Europe's aging demographic profile. The competitive environment is further shaped by the EU MDR, which raises the regulatory bar and reinforces the dominance of resource-rich incumbents capable of meeting stringent compliance requirements.

Beyond the top-tier players, several specialized and mid-tier companies maintain meaningful positions by targeting specific wound care segments, regional healthcare systems, or niche therapeutic areas. The Hartmann Group, based in Germany, is a prominent European-origin player with a broad wound care and infection management portfolio distributed widely across continental Europe. URGO Medical, a French company, has established strong clinical credibility particularly in the management of chronic wounds such as venous leg ulcers and diabetic foot ulcers, supported by an active European research presence. B. Braun Melsungen AG leverages its extensive European distribution infrastructure to compete effectively across hospital and outpatient wound care settings. Integra LifeSciences and Organogenesis contribute advanced regenerative and cellular tissue-based products, targeting complex wounds in surgical and clinical environments. Collectively, these players compete on dimensions of clinical evidence, product innovation, reimbursement compatibility, and health economic value-all critical factors in Europe's cost-conscious, outcomes-driven healthcare procurement environment.

The report provides in-depth competitive profiling of 15+ key players, including:

- Smith & Nephew

- Mölnlycke Health Care

- ConvaTec Group PLC

- 3M Company

- Coloplast A/S

- Hartmann Group

- URGO Medical

- B. Braun Melsungen AG

- Integra LifeSciences Corporation

- Organogenesis Inc.

- Hollister Incorporated

- Medline Industries, Inc.

- Medtronic plc

- Lohmann & Rauscher

- Winner Medical Group

Report Deliverables

- European and country-level market forecasts from 2025 to 2032

- Strategic insights into product innovation pipelines, regulatory developments, and reimbursement trends

- Market share analysis and SWOT assessments for key players

- Comprehensive segmentation by product type, application, end user, care setting, and technology

- Competitive benchmarking and strategic recommendations for market stakeholders

📘 Get Full Report Here:

Europe Advanced Wound Care Market - View Detailed Research Report

📥 Download Sample Report:

Europe Advanced Wound Care Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals, and healthcare infrastructure. Our research capabilities include:

- Real-time competitive benchmarking

- Global clinical trial pipeline monitoring

- Country-specific regulatory and pricing analysis

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us