Consumer Finance Market: Empowering the Modern Household through Flexible Credit

The Consumer Finance Market serves as the primary engine for individual purchasing power across the globe. By providing individuals with the capital necessary to manage immediate needs while spreading costs over time, this sector underpins the growth of the broader retail economy. In the wake of shifting global interest rates and evolving fiscal policies, the market has demonstrated remarkable resilience. Financial institutions, ranging from traditional banks to agile fintech startups, are increasingly focusing on delivering frictionless, user-centric experiences. As consumers demand more transparency and speed, the market is moving away from complex, paperwork-heavy processes toward instantaneous, data-driven approvals that empower households to achieve their lifestyle goals.

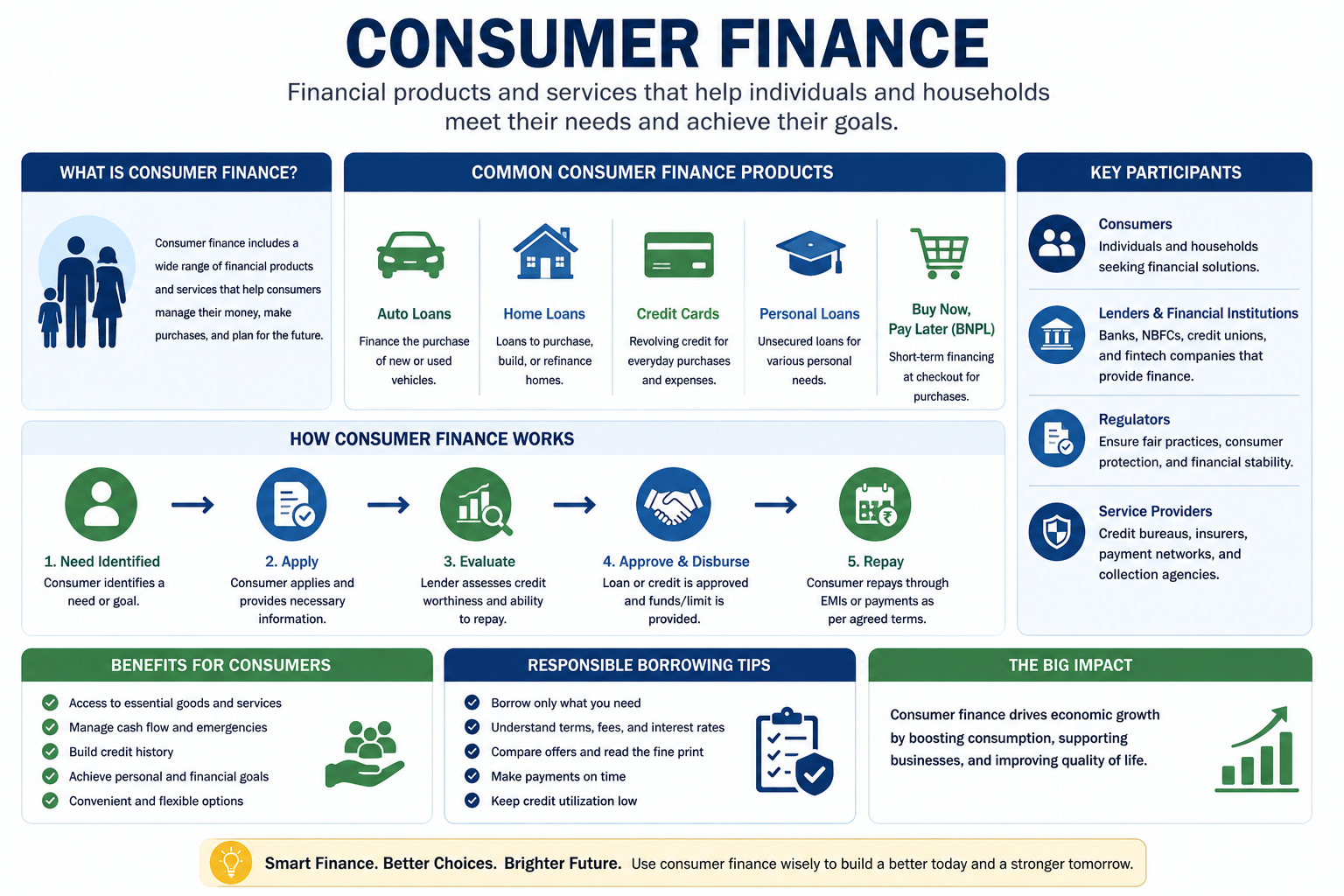

Market Overview and Introduction

The foundation of the consumer finance sector lies in its ability to bridge the gap between aspirations and affordability. Historically, this market was dominated by mortgage and auto lending, but the last decade has seen a dramatic expansion into unsecured credit and specialized point-of-sale financing. Today, the landscape is characterized by a high degree of diversification. Lenders are increasingly utilizing appliance financing loans to capture a larger share of the home improvement segment. Furthermore, the integration of consumer durable financing into both offline and online retail journeys has lowered the entry barrier for high-value purchases, ensuring that the market remains vibrant even during periods of cautious economic sentiment.

Key Growth Drivers

Several factors are propelling the expansion of the sector. The primary driver is the rapid urbanization of emerging economies, which has led to an increase in disposable income and a greater demand for a modern lifestyle. Additionally, the availability of comprehensive credit bureau data has allowed lenders to assess risk with greater precision, reducing the cost of borrowing for prime customers. The rise of "Buy Now, Pay Later" (BNPL) models has also introduced a younger demographic to structured credit, fostering a culture of disciplined, short-term borrowing that fuels retail consumption.

Consumer Behavior and E-commerce Influence

The digital revolution has fundamentally altered how people interact with financial products. E-commerce platforms are no longer just places to shop; they are becoming financial hubs. Modern consumers expect to see financing options at the checkout stage, seamlessly integrated into their shopping experience. This "embedded finance" trend has shifted consumer behavior toward smaller, more frequent credit applications rather than traditional, large-scale personal loans. The convenience of managing all financial obligations through a single mobile application has become a non-negotiable requirement for the modern borrower.

Regional Insights and Preferences

North America and Europe remain the most mature regions, with a heavy focus on credit card penetration and mortgage refinancing. However, the Asia-Pacific region is witnessing the most significant transformation. In countries like India and Vietnam, the leapfrogging of traditional banking infrastructure has led to a boom in mobile-first lending. Middle Eastern markets are also seeing growth in Sharia-compliant consumer financing, reflecting a demand for credit that aligns with cultural and religious values.

Technological Innovations and Emerging Trends

Technology is the most significant disruptor in the current landscape. Artificial Intelligence (AI) and Machine Learning (ML) are now used to analyze non-traditional data—such as utility bill payments and mobile phone usage—to provide credit to the "unbanked" or "underbanked" populations. Blockchain is being explored to enhance security and reduce the time taken for cross-border consumer transactions. Furthermore, the use of automated chatbots for customer service has significantly reduced operational costs while providing 24/7 support to borrowers.

Sustainability and Eco-friendly Practices

The rise of "Green Consumer Finance" is a defining trend. Lenders are increasingly offering preferential rates for loans used to purchase electric vehicles, solar panels, or energy-efficient home appliances. This not only helps consumers reduce their carbon footprint but also aligns the financial sector with global sustainability targets. Many institutions are also moving toward paperless operations, utilizing e-signatures and digital-only statements to minimize environmental impact.

Challenges, Competition, and Risks

Despite the positive trajectory, the market faces significant hurdles. High interest rates in several global economies have increased the cost of borrowing, which can dampen consumer demand. There is also the constant risk of cybersecurity threats and data breaches, which can erode consumer trust. Competition is fiercer than ever, with tech giants like Apple and Google entering the financial space, forcing traditional banks to accelerate their digital transformation or risk becoming obsolete.

Future Outlook and Investment Opportunities

The future of the market lies in hyper-personalization. We are moving toward a world where a credit offer is generated specifically for a person’s real-time financial situation and needs. Investment opportunities are particularly strong in the fintech infrastructure space—companies that provide the APIs and security layers that allow retailers to offer financial products. As regulatory frameworks evolve to provide better consumer protection, the market is expected to become more transparent and accessible to a global audience.

➤➤Explore Market Research Future- Related Ongoing Coverage In Semiconductor Industry:

Industrial Cooking Fire Protection System Market